Fets × IBEDC · 2022 – 2024

IBEDC

Care App + POS System

Built fragmented third-party portals into a unified billing system across digital and walk-in channels.

Unified how payments behave across channels — shared transaction logic, dual surfaces, and operational visibility at public-sector scale.

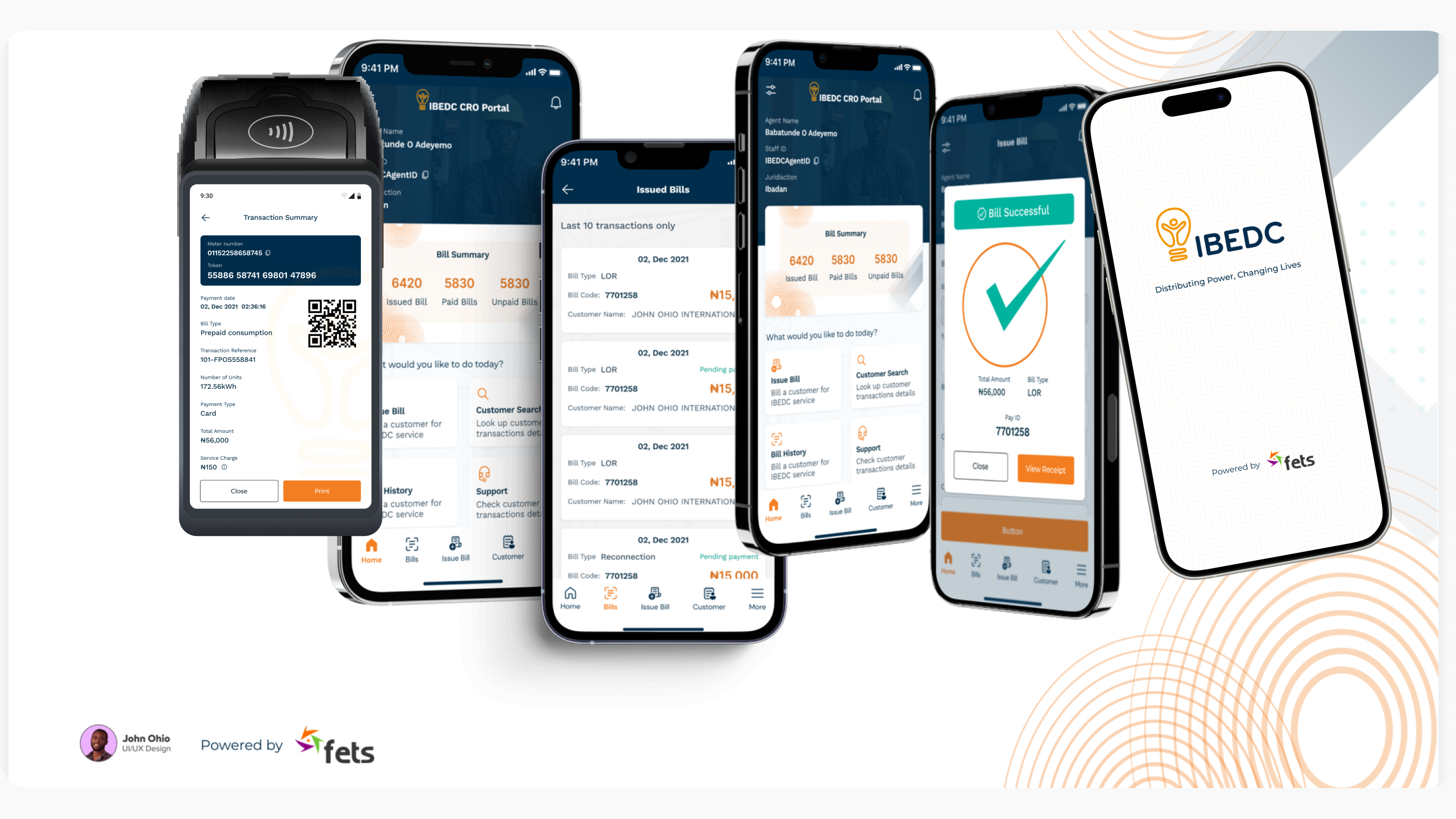

POS terminal workflow for walk-in centres

Unified transaction architecture across digital and in-person channels

Operational visibility and reconciliation model

IBEDC operations validation and field staff testing

- ·One billing system across channels

- ·Operations visibility before scale

- ·Field-ready workflows

02 Core Tensions

What made this hard

Three system failures that made fragmentation dangerous, not just inconvenient.

Digital and physical payment channels operated independently with no shared transaction logic. A payment started in one channel couldn't be verified or continued in the other.

Token delivery lagged 24–48 hours via SMS. In communities where power is managed by prepaid token, every hour of delay meant a household sitting in the dark after having paid.

Staff at walk-in centres had no real-time view of transactions. Fraud was undetectable, disputes unresolvable, and revenue leakage structural — because there was no unified record of what had been paid, by whom, and through which channel.

The solution was not to digitise payments, but to unify how payments behave across channels — regardless of where the transaction originates.

03 Evidence in practice

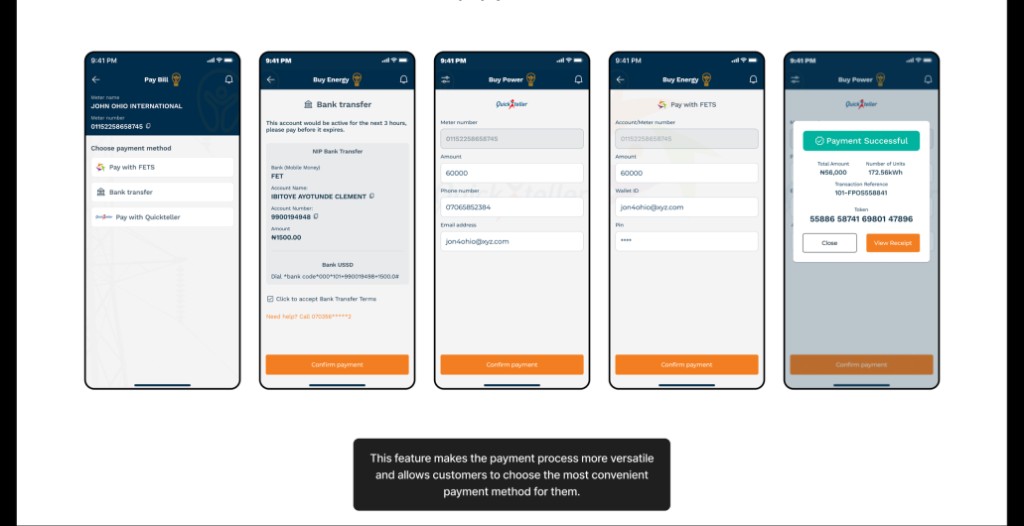

Self-service consumer experience: payment channel selection (bank transfer, Quickteller, FETS), token generation, and payment confirmation — designed for independent use without agent support.

Multi-channel payment flow unified under a single billing model — customers choose method, system resolves identically.

Figure 01 — IBEDC Care App: bank transfer, Quickteller, FETS, and payment success — multiple channels, one system.

- ·Dual-surface approach chosen over digital-only — walk-in customers represent the majority of IBEDC's 2.4M customer base

- ·Shared transaction logic makes the model transferable — same architecture deployed by 3 external utilities

- ·Field validation with IBEDC staff before rollout confirmed that design assumptions matched operational reality

Figure 02 — POS terminal interface: same transaction logic, different surface.

- ·Agent-assisted workflows were designed to continue transactions, not restart them

- ·Receipt and verification surfaces anchored to the same transaction record as the consumer app

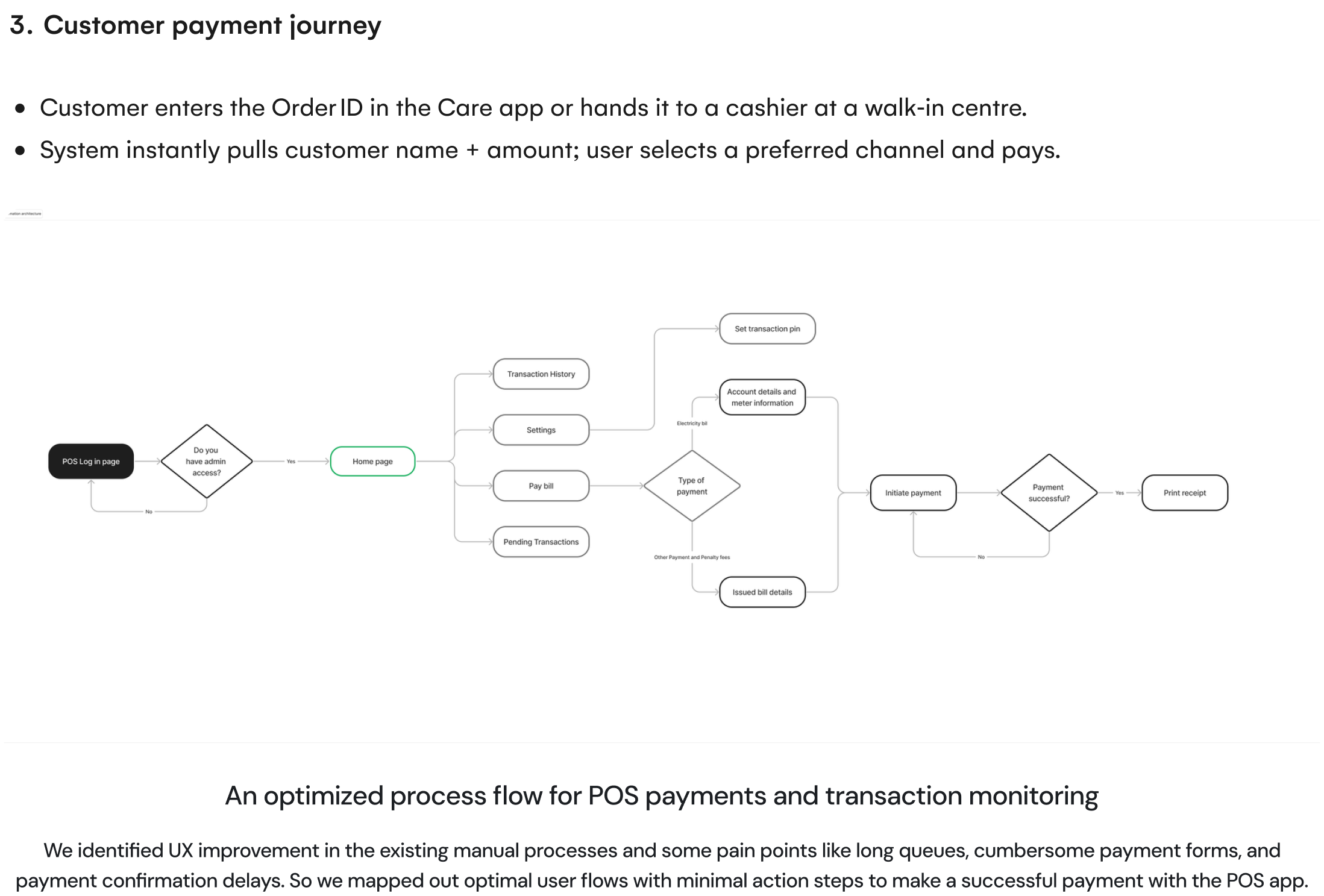

Walk-in centre operations: agent login, bill lookup, payment initiation, and receipt printing. Agents step in and continue any transaction without switching systems or reprocessing.

POS terminal workflow built on the same transaction logic as the app — agents and customers operate from one shared system.

Token delivery became immediate. Transactions visible to staff at point of interaction. Disputes resolvable without escalation.

Unified transaction record made reconciliation auditable across every channel — fraud detectable, revenue trackable.

Figure 03 — Customer journey: self-service and agent-assisted flows sharing the same underlying transaction logic.

- ·Real-time states reduced call-centre load by making token delivery and payment confirmation visible immediately

- ·Unified record closed reconciliation gaps that enabled fraud and revenue leakage

05 Outcomes

What the system delivered

06 Foundations

The dual-surface model — validated at 2.4 million customer scale — established the template adopted by three external utilities without rebuilding from scratch.

Shared transaction logic proved that digital and physical payment channels don't need separate systems. The same principle now applies to every utility operator that adopted the POS template.

IBEDC was the first implementation. The operational model — shared logic, dual surfaces, real-time visibility — is the template.